In this episode of the Fintech Fun podcast, Chris Titley chats with Michael Ragavan, founder of Our Leg Up, a revolutionary financial service aiming to tackle wealth inequality by making homeownership more accessible. Michael shares how Our Leg Up enables aspiring homeowners to purchase properties with just a 5% deposit, eliminating the need for lenders' mortgage insurance and providing competitive interest rates. He discusses the platform’s unique partnership model that connects equity-rich investors, banks, and aspiring homeowners, all while mitigating financial risks. Michael also touches on the challenges of educating the market, the role of partnerships in scaling, and the company’s global aspirations. Tune in to hear how Michael’s innovative approach is redefining the Australian dream of homeownership and how AI is playing a role in streamlining the process.

Our Leg Up: Platform enabling aspiring homeowners to purchase property with a 5% deposit.

AI in Financial Services: Used for risk assessment, customer support, and secondary analysis.

Basel III Framework: Underpinning the scalability of Our Leg Up across 100+ countries.

Carnatic Drums: Michael’s early foray into music and stress relief.

Transcript Synced · click any line to jump ▾

Chris Titley: You're listening to a Day One FM show.

Michael Ragavan: Pick My Brain is the podcast where founders pitch me their startup and I try to give them some useful advice so they can connect better with potential co-founders, investors, media, and of course, customers. My name's Alan Jones and I was a founder myself for about 15 years, and after that, an angel investor for another 15 years. So yeah, old. Some of my ventures have been successful and some failed disastrously,, but I like to think I've learned a thing or two along the way and maybe some of that can help you. So if you'd like to learn how to tweak your pitch, subscribe to the Pick My Brain show now wherever you like to listen to podcasts.

Speaker C: Hi, it's Chris Tittle here as part of the FinTech Fun episode. I'm joined by Michael Ragavan, founder of Allegup. Michael, thank you so much for joining us and I know you are joining us live here from Mexico today.

Chris Titley: Yeah, that's right. That's right. Just in Cancun for a few days. Yeah, thanks for the invite.

Michael Ragavan: Excited to be here. Michael. Yeah, no, Absolutely, Michael.

Speaker C: I'm curious to know for the listeners out there that know nothing about Owlegup, can you go back to the origins, the history of the business, how the business began and what it does?

Chris Titley: Yeah, sure. So formerly I was a mortgage broker, investment banker, and an investment advisor. I quit all that about 3 years ago, start building Owlegup. And so at a high level, we're on a mission to diminish wealth inequality. And the number one driver of that in Australia is not owning a home. So for most Houses are their largest asset, most important wealth accumulation vehicle, but there's a big barrier standing in the way and that's saving a 20% deposit. So that's why we're building Australia's surrogate bank at moment. It means aspiring homeowners can purchase property with as little as a 5% deposit at the same interest rate as a 20% deposit and they save on lenders mortgage insurance. So they're getting in 5, 10 years faster, saving tens of thousands in the process.

Speaker C: Awesome, mate. And obviously with COVID we saw a bump in property prices and it has become much more unaffordable for the Australian dream. What is the Australian dream now? Do you think it's unachievable or achievable?

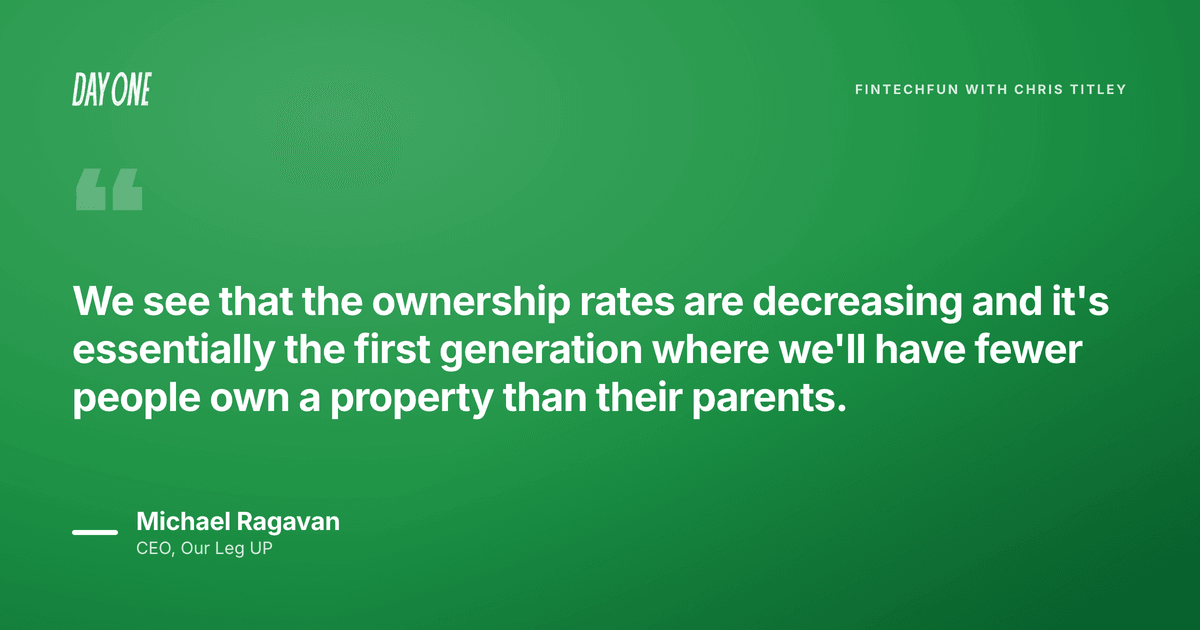

Chris Titley: We see that the ownership rates are decreasing and it's essentially the first generation where we'll have less people owning a property than their parents. And so of course that's not great in terms of comparative wealth and financial security. But I think that there are new solutions coming into the market and what matters is which ones align with you. The government's done a few things, banks try to help, but I think it's these new financing models and affordability models that are going to make a difference and keep the other dream alive.

Speaker C: There's a lot of moving parts to OurLegUp, I'd assume, and in terms of who the customers are, can you give a bit of a snapshot of how you've built this business and how you're going about sort of managing all those moving parts?

Chris Titley: Yeah, sure. So it did feel a bit complicated early on, but what we got down to was a coordination between established homeowners, so essentially investors who are acting as part of that surrogate bank of mum and dad, lenders that we partner with, and then of course their customers being aspiring homeowners. What we end up doing is taking registered charges from the investors. And so the value proposition for them is they're able to make a return on inaccessible equity sitting in their property without any capital outlay. So that's a world's first, and it took us 18 to 24 months in terms of our financial engineering and, and all the legal hurdles. But essentially we take these charges and we allocate them to our partner lenders. So that when they go off and do low deposit lending individually and in aggregate, the LVR of the loan sits below 80%, and that's where they get their benefit from. So for the banks, we allow them to offer these reduced interest rate home loans with less risk and improved margin. And of course, for the aspiring homeowner, which is their customer, they're able to purchase a property for tens of thousands less because of the better interest rate and less fees.

Speaker C: Right. And from an investor point of view, are you targeting a particular number or a return, or can you do that, or is that allowed?

Chris Titley: Yeah, yeah, sure. So it's not a fixed income product. The return is more akin to a dividend return paid out quarterly. Across cycles, it's about 4% per annum. And in terms of who we're targeting at the moment, it's very much for sophisticated investors with equity in their property. And then eventually, hopefully we can make it available for retail investors. But in terms of launch, it'll be limited to that for now.

Speaker C: And in terms of the geographic spread of OurLegUp, are you aiming to be in a particular state, city, or even potentially global aspirations?

Chris Titley: Yeah, sure. So we are starting off in Australia and it will depend on the footprint of the lenders that we partner with. And so we're happy to be across the country. We've done our modeling for that. And of course, aspiring homeowners need to pass the bank's credit policy anyway before we're able to support the loan because we're very much service for the bank that ends up benefiting the aspiring homeowner. In terms of aspirations, I think there's a few things. So this is the first use case for the inaccessible equity, but we really want to be an exchange that unlocks the inaccessible equity as a force for social good. And so we're also looking at green home loans. We're also looking at corporate debt, commercial debt, and because it's built on the Basel III global banking framework, it is applicable across over 100 countries.

Speaker C: Right, excellent. And I suppose every now and then we have some macro shocks and things don't go to plan and we saw it in 2008 with the GFC and then 2020 with COVID How are you prepared for something like this in terms of your modeling and in terms of the understanding of the products that people have that things don't go a bit pear-shaped?

Chris Titley: Yes, you're right. So in the Hayne Royal Commission, there was a crackdown on guarantor home loans and rightly so because of the financial risk it placed on guarantors without any financial reward. So When we were thinking about building out this product, there was sort of two things. One, it needed to be low risk enough for us to place our parents in. And the other one was that it needed to provide a decent return, not just charitable intent. So I think the 4% per annum, that's essentially cross-cycles and it's on lazy equity. So essentially 4% more than what you can currently get. And then in terms of the risk profile, the high-level takeaway is that 1 in 10 of the loans supported would need to default, foreclose, and must be liable for the maximum amount of negative equity for any of our investors to lose a dollar net. And so that's a magnitude more than what happened in the US during the GFC. And it's because we've built out 5 key risk mitigating mechanisms. And yeah, we essentially go through that process with our investors, make sure they understand the risk profile before they sign the dotted line.

Speaker C: And Michael, in regards to building out your team and also the growth of your own business, can you talk about that? I suppose some challenges and also some wins that you may have had.

Chris Titley: Yeah, sure. So in terms of building out the business, I mean, we've been in incubation for about 3 years. October '21 is when we incorporated and Outroadus, our first check, and then we did a small round off the back of that. And it's largely been that round that's been funding us all this time. So we're pretty lean. We're about 5 FTE across 8 people and we're yet to generate revenue. And so it's been quite a rollercoaster of a journey. We've had to keep quite lean and have sort of fraction of employees here and there that helps spur the business along and make sure we have the right expertise at the right time, whether that's legal, financial, regulatory, developing partnerships with banks. But we are on the cusp of monetization. So I think the exciting thing is we'll be in market by the end of next year and generating revenue. And so from that point on, we'll be able to scale the team out a bit more. But until then, we've been pretty lean.

Speaker C: And Michael, what's the ask for the community out there, I suppose? Is there anyone out there that you'd like to listen to this podcast that should reach out to you? What type of people are you targeting?

Chris Titley: Yeah, sure. So perhaps a couple of things. One is that we'd love to talk to people either in banks or non-banks around home lending who could help us scale partnerships on that side. And the other thing is right now we're going through, we've been building out the amount of equity commitments we have largely directly. So we have about $40 mil worth of commitments and that will be able to support $250 mil worth of home loans. But we'd like to scale through partnerships with wealth managers, brokers, rental companies. So yeah, people in that space would love to chat as well.

Speaker C: Yeah, how important is that partnership model play for you in regards to the amount of people that can talk about your product, distribute your product, and understand your product, and then be a sales advocate?

Chris Titley: Yeah, you're right. So one of the hurdles we anticipated was educating the market because we don't want to seem like we're selling magic beans because we're not. There's of course risk involved and it's helping someone understand that. And so right now the minimum commitment's about $250,000 and for someone to— worth of equity. And for someone to understand that, they want you to chat to them for at least half an hour to an hour. We were able to get about $20 mil without spending a dollar on customer acquisition. But moving forward, we're not gonna be able to spend that much time for each customer. And so we want financial advisors or brokers, essentially trusted advisories that we can educate about the product, who are able to see if it's suitable for their customers and bring them on. And we've got a referral model to make sure that everyone gets a piece of the pie for that.

Speaker C: Yeah, yeah, no, for sure. And then it wouldn't be a podcast in 2024 without talking about AI, mate. AI and financial services and AI when it comes to prop tech. What's your views in terms of threat or opportunity?

Chris Titley: Opportunity for sure. I've noticed that our developers have been much more productive, first from the US.

Speaker C: Yeah.

Chris Titley: And just building out the platform for doing secondary risk assessments. So that's one place we can use it. The other is of course, investor services, customer support. And then the other place is even with our risk assessment modules, being able to make those a lot more comprehensive through AI. So those are probably the 3 areas we're looking at at the moment.

Speaker C: And Michael, you're in Mexico at the moment. When you're not talking about modeling property prices or modeling yields or investments or whatnot, do you get a chance to switch off? Are you on holidays at the moment or are you working from Mexico?

Chris Titley: That's a good question. So I'm accompanying my wife who's going to be into the US to do a research presentation, and so Mexico was a quick stop before we went there. It is a combination between a holiday and a bit of work. That's just the reality of being a founder sometimes. You have these natural ebbs and flows, and I think towards the end of December, start of February— I mean, start of January— there's a bit of a natural lull, so we'll take advantage of that. But otherwise generally working. In terms of what I tend to do outside of modeling these exciting scenarios, one would be playing soccer. I've done that all throughout high school and uni. The other one's playing music. So I'm a drummer, quite enjoy that as well. And the last one is probably spending time at church.

Speaker C: Yes. Yeah. And so on the soccer front, do you get annoyed when people call it soccer and not football?

Chris Titley: It's a good question. I call it soccer, but I think because I'm from Australia, I do get annoyed when people call it football because my reference for football is very different. Yeah. Yeah.

Speaker C: What's your football is it league or union or Aussie rules?

Chris Titley: It's Aussie rules.

Speaker C: Aussie rules, yeah, no, for sure. Mine too. And then on the music, the drumming, where did that come from? A bit of early childhood?

Chris Titley: Yeah, that's right. Around 6 years old, I think. Initially started out playing the Karinatic drums and then also just regular drum kit. And I've been playing that essentially throughout uni, even a little bit after uni, playing with the music academy, playing for churches, things along those lines. So I've always enjoyed that and I find it quite good in terms of strategy.

Speaker C: And what about watching soccer? Do you soccer watch or are you a soccer player?

Chris Titley: I'll admit I'm not as much of a watcher, mainly playing in real life and then also a bit of FIFA.

Speaker C: Yeah, right, on the Xbox or PlayStation?

Chris Titley: On the PlayStation, yes.

Speaker C: Yeah, right. And favorite particular player or team that you play with on the Xbox?

Chris Titley: So I think a little bit controversial, but Real Madrid.

Speaker C: Oh, well, not really. I mean, it's a well-known brand, I suppose. One of the global— It's a polarizing team. Maybe if you're in Spain as well. Yeah. And Michael, we do this interview in 12 months' time, we repeat this and we look back on this interview. Where do you think the business would be or want to be? And I suppose, what are the plans?

Chris Titley: Sure. So plan is to be live in market by the middle of the year and support roughly 50 properties to 100 properties or purchases essentially. And so we currently have capacity to support about 20 properties. 500, but I think within the 6-month span, the goal is to support 50 to 100. So hopefully we'll be able to look back and say we're, uh, close to break even at that point.

Speaker C: Yeah, amazing. And then on the funding front, are you looking to get some funding yourself, or are you hoping to sort of bootstrap your way through?

Chris Titley: Yeah, it's a good question. I think that's the next major milestone will be once we're out in markets. Uh, when we initially raised about 3 years ago now, there were 5 milestones we wanted to hit. We hit those, but we got to a solid value inflection curve and then we've been raising off the back of that. And so that's due to close by the end of this year and don't anticipate to need to raise following that unless it's to pursue growth opportunities.

Speaker C: Yeah. Excellent, Michael. Well, mate, thank you so much for giving us an understanding of ourLegUp, how the business began through a problem that you see, which is to me sounds like it's not going away. And in regards to allowing people to sort of alleviate a little bit of cost of pressure of the cost of living as well, which is a bit of a crisis going on as well. All the best in the coming year. A big year for you, as you mentioned.

Chris Titley: Yes.

Speaker C: In regards to the launch in 2025, let's hope it's a prosperous year and looking forward to following the progress and catching up.

Chris Titley: Definitely. Thanks for your time, Chris. Look forward to giving you all the update.

{kind=link}